Continuing the “Top 10” economic issues being discussed in this column, this 8th installment will tackle one huge elephant in the room, the ever-rising taxpayers’ burden which is the military and uniformed personnel (MUP) pension system.

Here are 10 issues that Philippines taxpayers and public finance researchers should consider.

1. Government civilian personnel contribute for their future pension, MUP do not. Government doctors, nurses, teachers, engineers, agriculturists, etc. Accept the additional deductions from their monthly pay that go to the Government Service Insurance System (GSIS), the MUP do not. Taxpayers pay for active service MUP salaries and other compensation, then when they retire, taxpayers again have to pay for their pension — and the scheme is egregious.

2. The amount is huge, P65 billion/year a decade ago, P130 billion this year. In an article written a decade ago by Benjamin Diokno (now Finance Secretary), “Military Pension,” (BusinessWorld, Aug. 13, 2013), he observed and presented the numbers (see Table 1).

“The uniformed personnel of the AFP, the DILG, NAMRIA and the PCG [Armed Forces of the Philippines, Department of Local Government, the National Mapping and Resource Information Authority, and Philippine Coast Guard] have to rely on direct appropriations by the National Government. Why? Because the military’s pension fund collapsed a long time ago as an aftermath of the Asian financial crisis and the financial mismanagement of their respective retirement funds.”

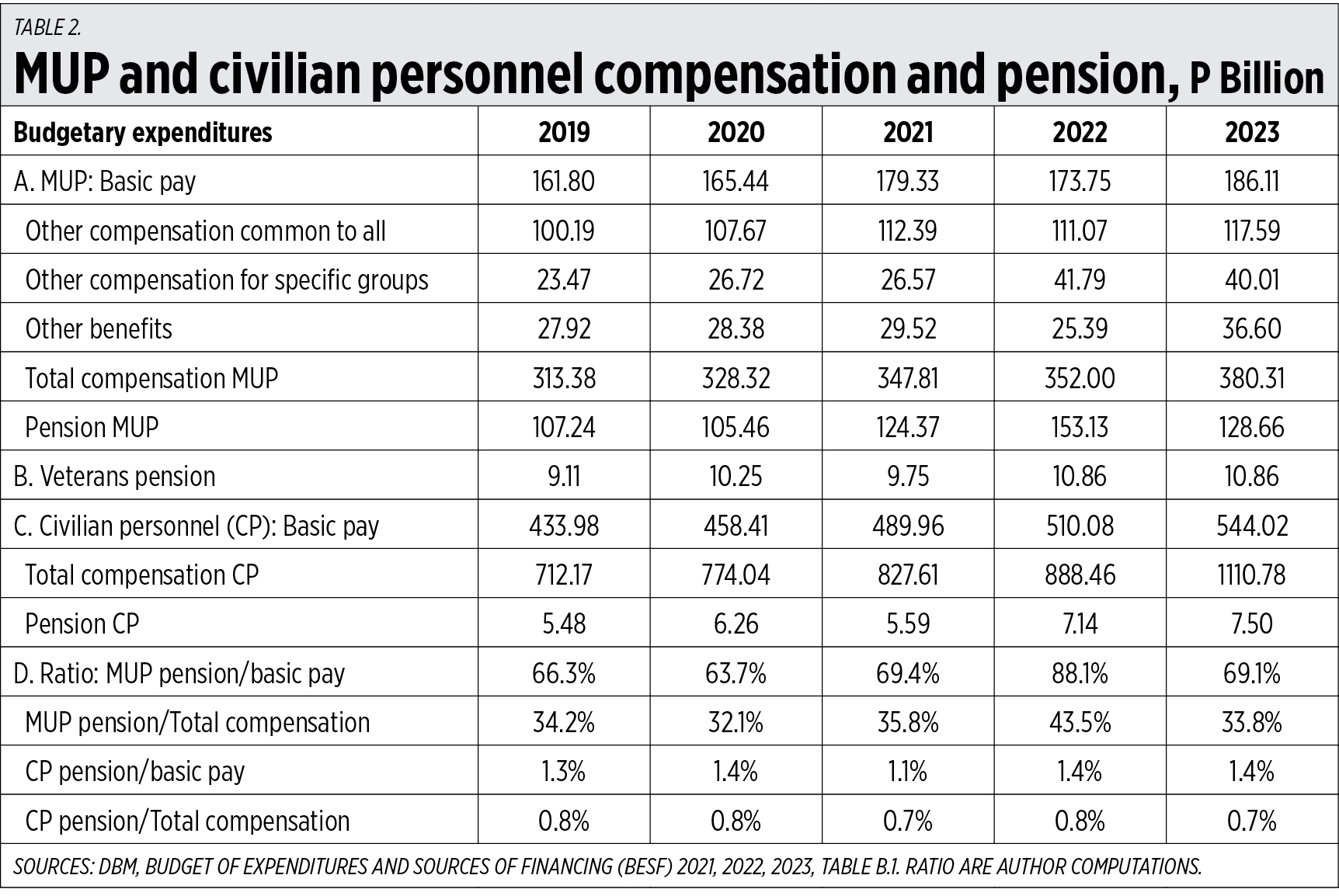

3. MUP pensions are up to 88% of base pay of active soldiers, policemen. The share of MUP pension/base pay averaged 66.5% in 2019-2021, then jumped to 88% in 2022. In contrast, the civilian personnel pension/base pay averages only about 1.3%. Including various allowances, hazard pay, etc., MUP pension/total compensation averaged 34% in 2019-2021 then jumped to 44% in 2022.

4. MUP in active service already get generous pay, averaging P335 billion/year in 2019-2022. In Table 2, “Other compensation common to all” includes longevity pay, subsistence allowance, relief allowance, mid-year bonus, year-end bonus, and others.

“Other compensation for specific groups” includes combat duty pay, combat initiative pay, hazardous duty pay, lump-sum for filling of positions MUP, others. And “Other benefits” include terminal leave, retirement gratuity, and PhilHealth contributions, others.

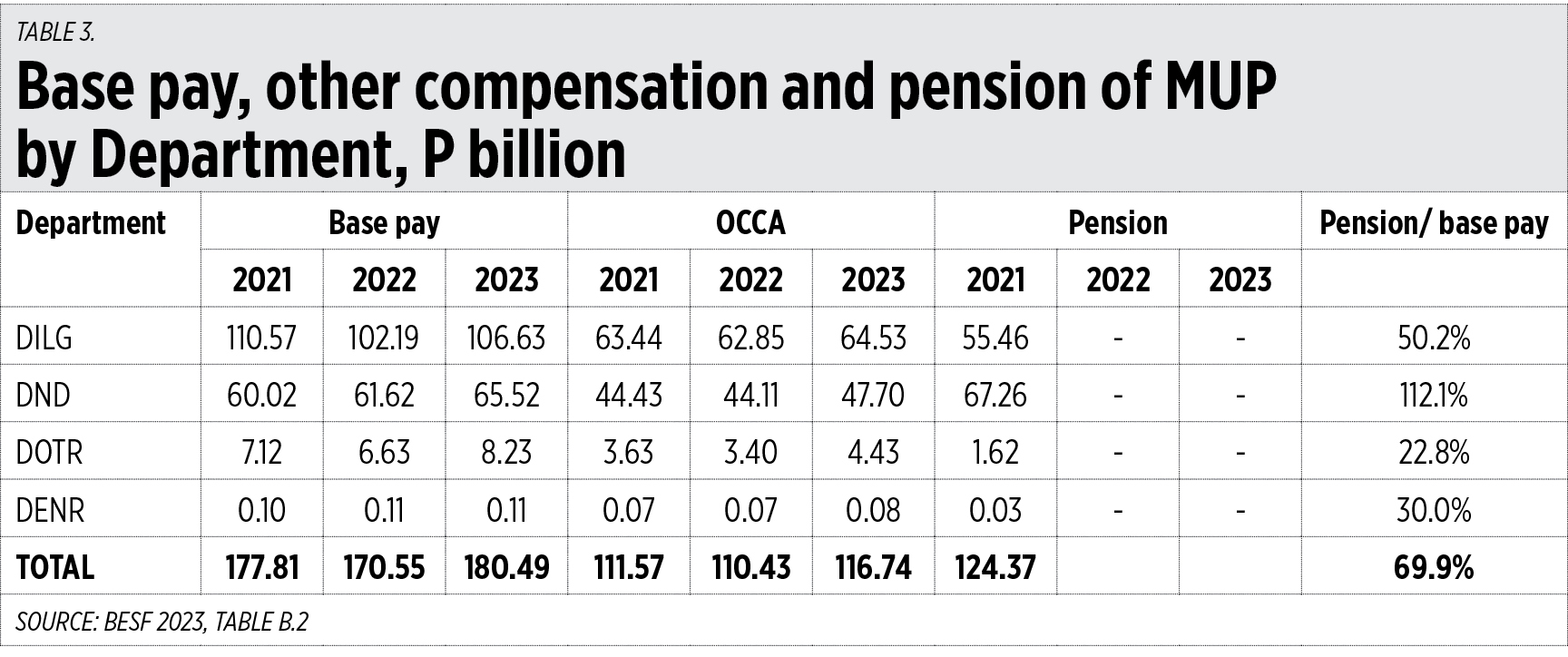

5. MUP under DILG have larger base pay than the Armed Forces of the Philippines-Department of National Defense (AFP-DND) but have lower pensions than the AFP. From 2021-2023, the average base pay of MUP in the DILG was P106 billion/year while base pay in the AFP-DND was P62 billion/year. But the pension of MUP in the DILG was only P55 billion in 2021, lower than the P67 billion pension in the DND.

6. The AFP pension is larger than base pay of active soldiers. In 2021, the pension in the AFP-DND was 112% of base pay while the Philippine National Police (PNP) pension was 50% or one half of base pay of active policemen. The average for all MUP was 70% of base pay (Table 3).

7. An AFP pensioner can get P191,000/month for life. Consider these two recent columns in BusinessWorld: “The Game of the Generals” by Amelia H. C. Ylagan (Jan. 22, 2023) and “Dealing with a looming military pension crisis” by Victor S. Limlingan (Oct. 18, 2022).

Ms. Ylagan wrote, “A retired (full) General can get lifetime pension of up to P190,975.88 per month, computed on 85% of highest base pay plus longevity pay for the maximum number of years served. (The pension lowers as the rank lowers, with the lowest, Brigadier General, still getting about P100,000 per month pension or close to this.)”

Mr. Limlingan wrote, “The GSIS actually did an actuarial study of the financial impact of absorbing the military and estimated that this would involve assuming P9.6 trillion in unfunded liabilities, clearly beyond the financial capacity of the GSIS. And so the problem looms… Our Congressional Planning and Budget department estimates that if no reform is undertaken, the National Government will need P800 billion for the next 20 years.”

8. The Development Budget Coordination Committee (DBCC) of previous and current administrations rang the bell on MUP pension. The DBCC — a.k.a. the “economic team” composed of the heads of the Department of Finance (DoF), the Department of Budget and Management (DBM), the National Economic and Development Authority (NEDA), and the Bangko Sentral ng Pilipinas (BSP) — of both of the Duterte and Marcos Jr. administrations raised the alarm bells on this huge fiscal burden. Consider these reports in BusinessWorld:

“Gov’t facing P9.6-trillion bill for military pension obligations” (Feb. 2, 2021),

“Economic managers back military pension reform” (June 16, 2021),

“GSIS deemed stable despite AFP pension risk” (Dec. 5, 2021).

From the Dec. 5 report: “An actuarial study by the Department of Finance concluded that the creation of a retirement fund solely for military and uniformed personnel will require an additional P45 billion annually.”

9. Suggested Reform No. 1: All MUP in active service should contribute to GSIS. Among the important reforms advocated by the DBCC and other concerned groups is that the MUP should pay for their own retirement pension. And there is no need to create another agency to handle this — GSIS can handle civilian pension and MUP pension. I say “amen” to this. The MUP pension should not come from taxpayers again as they are already over-burdened. Think of the P2 trillion/year of new borrowings for three years, 2020-2022, the taxpayers will ultimately pay for that.

10. Suggested Reform No. 2: Scrap, abolish the indexation of pensions on salaries of the incumbent, not the retiree. As Mr. Diokno wrote in 2013, “Well, during the final months of the Fidel Ramos (FVR) presidency, he approved what I consider to be the most generous pension system for the military in the entire world. While the common practice is to base the pension benefits on the highest salary (usually the last) of the retiree, under the law approved by Mr. Ramos, the pension is based on the salaries of the incumbent. Absurd but true.”

Again, I say “amen” to this reform. I admired and praised former President FVR’s handling of the economy — see this column’s piece, “The Post-SONA Economic Briefing; FVR’s economy” (Aug. 1, 2022) — but such admiration is now diminished. But if he was alive today, I think he would be among the reformers who would call for the scrapping of this egregious scheme.

I hope that MUPs in active service in various departments and agencies will not resist these two reforms. Their motto, to “serve and protect,” should refer more to the public and taxpayers, not to themselves and their future pensions.

I also hope that the public and other media also begin to discuss the elephant in the room. The amount is so huge. People were scandalized by the Education department’s laptop overpricing scandal in the previous administration, estimated at P0.96 billion. And rightly so. But the MUP pension, like the P153 billion in 2022 budget, should have not been there in the first place and it is a huge hole in taxpayers’ pockets.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers.

{kind=link}

{kind=link}

{kind=link}