Three bills were filed at the House of Representatives at the First Regular Session of the 19th Congress proposing to amend the mining taxes, among other purposes. Except for House Bill (HB) 373, which applies to both large- and small-scale mining, HB 2014 and HB 2246 cover only large-scale metallic mining operations.

These bills are responses to the call of the late President Benigno Aquino III during his 2012 State of the Nation Address (SONA). He articulated the concerns of some quarters of the country regarding the large-scale mining industry delivering less than its fair share to the government of the revenues obtained from extracting the country’s mineral resources. In that SONA, the former President cited how the government obtained only 9.2% of the revenues. With Executive Order (EO) 79, he declared a moratorium on new mining projects until Congress passes a new mining tax reform law. The Tampakan copper mining project in South Cotabato has not been granted permit because of EO 79, and the country has forgone the benefit from that project.

The three bills propose to introduce a flexible revenue sharing arrangement. HB 2246 prescribes the government’s share to be 10% of gross revenue or 55% of the adjusted net mining revenue (ANMR), i.e., gross revenue net of allowable deductible expenses, whichever is higher. In the event ANMR exceeds 50% of gross output, the government gets 55% of the threshold ANMR, which is 50% of gross revenues, plus 60% of the excess ANMR over threshold ANMR.

HB 373 and HB 2014 propose royalty payment obligations of large-scale mining companies at 3% on gross output for those operating in mineral reservations, and graduated rates on the profit margin of companies outside mineral reservations. The graduated rates range from a percent to 5%, where profit margin is the ratio of income before corporate tax to gross revenues. The highest royalty payment of 5% applies to profit margins above 70%.

All three bills are responsive to the call of former President Aquino for Congress to introduce a tax regime that would let the government capture its fair share of mining revenues. When prices of metals increase in the world market, the royalty payments go up to increase the share of government. Just before the SONA of former President Aquino, metal prices were high.

According to the late President, “In 2010, P145 billion was the total value derived from mining, but only P13.4 billion or 9% went to the national treasury. These natural resources are yours; it shouldn’t happen that all that’s left to you is a tip after they’re extracted.”

But what if metal prices plunge? All three bills fix minimum royalty payments at 5% of gross revenues. When metal prices are low, gross revenues go down while operational costs remain high reducing the net income from mining. On this side of the business cycle, it is now the mining companies which face the higher burden of the mining tax regime.

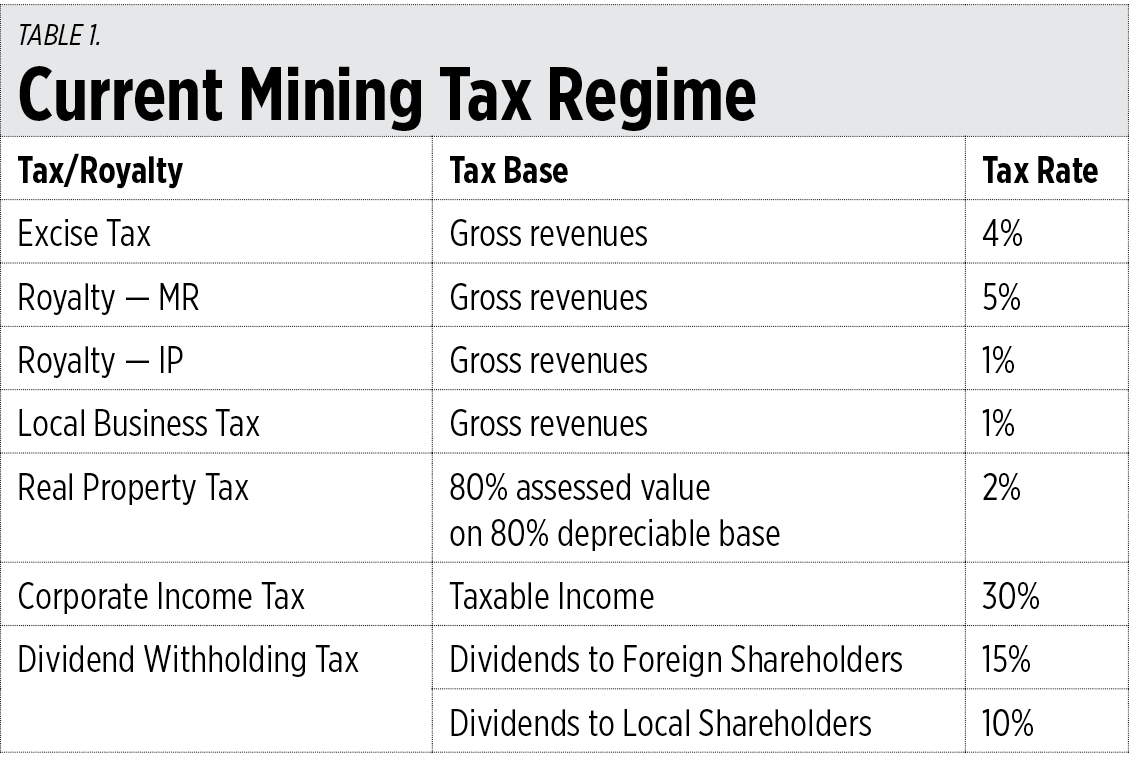

To pursue this point further, one may use the average effective tax rates (AETR) to be the indicator describing the impact of the fiscal regime. Setting aside for now the proposed tax reforms introduced by the above bills, Table 1 shows the current tax regime. I note that the recent TRAIN (Tax Reform for Acceleration and Inclusion) law increased the excise tax rate from 2% to 4%.

The AETR of a mining activity is the present value of the tax collections from year one to the last year of the project divided by the present value of the stream of income before taxes. A typical price of the metallic product, say, copper, is used to value the output throughout the project.

In Table 2, an average copper price was used to compute these AETRs of the various types of copper mining contracts. Copper mining by a company under a financial or technical assistance agreement with the government (FTAA) and operating in ancestral domain (AD) has an AETR of 102.66%. The same contract with accelerated depreciation and tax holidays has a lower AETR at 83.87% and 67.18% respectively. Companies with mineral production sharing arrangements (MPSA) have AETR at 75.65%. Their AETRs increase to 78.44% and 92.43% if they are in ancestral domain and in a mineral reservation and ancestral domain, respectively.

A general observation is that the AETRs for copper in other countries are lower than in the Philippines. Countries with comparable AETRs as ours include the United States, Russia, Peru, and Canada. Those with relatively low AETRs include Mexico, Indonesia, Chile, South Africa, Australia, and Brazil.

The Mineral Industry Coordinating Council (MICC), which EO 79 created, proposed the highest revenue sharing arrangement, which was 10% of gross revenues or 55% of ANMR, whichever is higher. The AETRs of the MICC proposal are computed at 51.4% and 122.52%, respectively.

The three mining tax reform bills apparently picked up from the proposal of the MICC. But there are important improvements. The graduated profit tax rates of HB 373 and HB 2014 are important refinements to the MICC proposal.

But the more interesting improvement is in HB 2246. It picked up the MICC proposal but added that payment of the prescribed royalty payment is in lieu of all national and local taxes including the income tax, royalty for indigenous cultural communities, duties on imported specialized capital mining equipment, fees for mayors and or business permits, and other fees and shares imported by the host LGUs. Apparently proposing a PEZA-like fiscal regime for large scale mining operations, this bill has the added feature of simplifying mining taxes.

Going back to the business cycle, the above AETRs were computed using an average price of copper. A typical mining project may run for two decades, and within this time period metal prices can fluctuate. If these AETRs are computed using high prices of metals, the mining companies tend to get the larger part of the revenues. However, if low prices are used, the government gets the bigger share.

The lesson here is that fair sharing of revenues from large scale mining operations requires symmetrical royalty payments along the business cycle. If the above mining tax reform bills have each introduced features for the government to capture its fair share as metal prices go up, the proposals should likewise add arrangements of reducing the burden to mining companies in depressed metal markets.

Ramon L. Clarete is a professor at the University of the Philippines School of Economics.

{kind=link}

{kind=link}