(Third of four parts)

The government economic team or the members of the Development Budget Coordination Committee (DBCC) will hold another Philippine Economic Briefing (PEB) today in Singapore with a clear goal of attracting more foreign investments to create more jobs in the country. The economic team also went to Singapore and Jakarta for the first PEB in the second week of September last year.

Very likely among the important announcements to be made by the team will be on the recently enacted economic liberalization measures like the Public Service Act Amendment and Retail Trade Liberalization, the proposed Maharlika Investment Fund, and taxation policies.

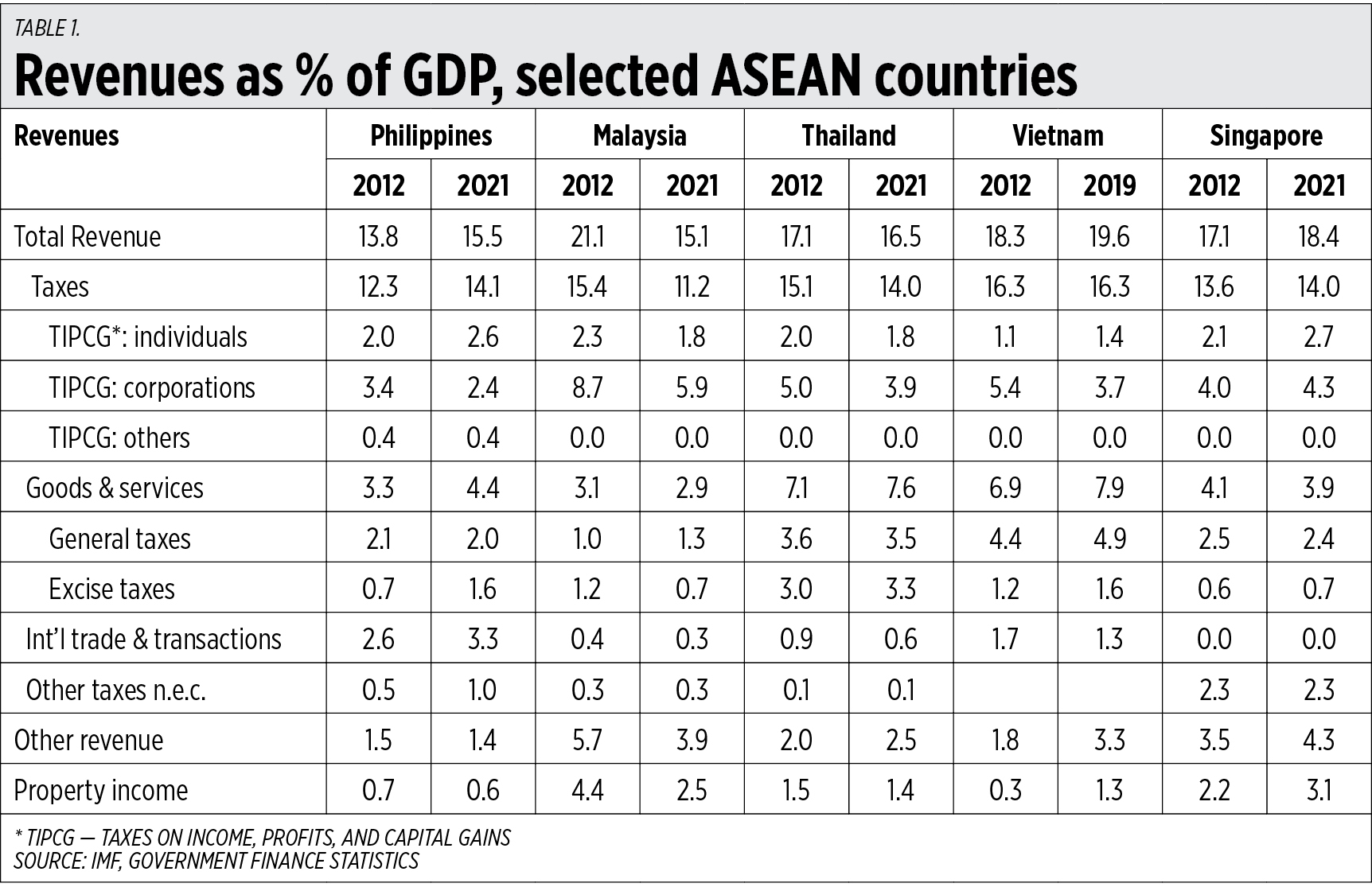

I checked the revenues/GDP ratio of some ASEAN countries and saw that the ratio is generally similar among them — 15-18% in 2021. Vietnam’s was 20% in 2019 but there was no data for 2021. Note that this is for National Government revenues alone and does not include the revenues of local government units (LGUs) as they have their own local taxes, fees, and other sources of income. If LGU revenues are included, overall revenues/GDP ratio can easily rise to 16-17%.

One notable thing in the Philippines’ tax policy is that it imposes relatively high taxes on international trade, both exports and imports, at 3.3% of GDP. Whereas Singapore has zero, Malaysia has only 0.3%, Thailand 0.6%, and Vietnam 1.3%.

The Philippines has the highest VAT rate in the ASEAN at 12%, yet its revenues from general taxes including VAT is low, only 2%, while Thailand and Singapore with VAT rates of only 7% and 8% have general taxes revenues of 3.5% and 2.4% respectively (see Table 1).

Finance Secretary Benjamin Diokno has acknowledged the problem in the country’s VAT system. He noted that from 2016 to 2020, the Philippines collected an average of P723 billion from VAT, which is just 0.40 of the expected VAT collection. The ASEAN average is 0.57 — Thailand has the highest VAT efficiency at 0.79, while Singapore has 0.71 efficiency.

Mr. Diokno has attributed the low efficiency to the many VAT exemptions granted by the government in various sectoral laws. He is correct and I believe reviewing those VAT exemptions should have been done yesterday, or at least today.

Here are recent tax-related reports in BusinessWorld: “Government urged to consider inflation impact of new taxes” (May 14), “Excise tax collection below target due to illegal tobacco — BIR” (May 18), “Tax reforms generated P202.8B in revenues in 2022” (May 29), “PHL posts lowest VAT efficiency in region” (May 31), “Gov’t warned against overdependence on ‘regressive’ sin taxes” (June 4), “Tax system being outmaneuvered by digital companies” (June 5), “PHL needs a more ‘dynamic’ excise tax regime — solon” (June 5), “EV industry lobbying for incentives to support new-vehicle adoption” (June 13).

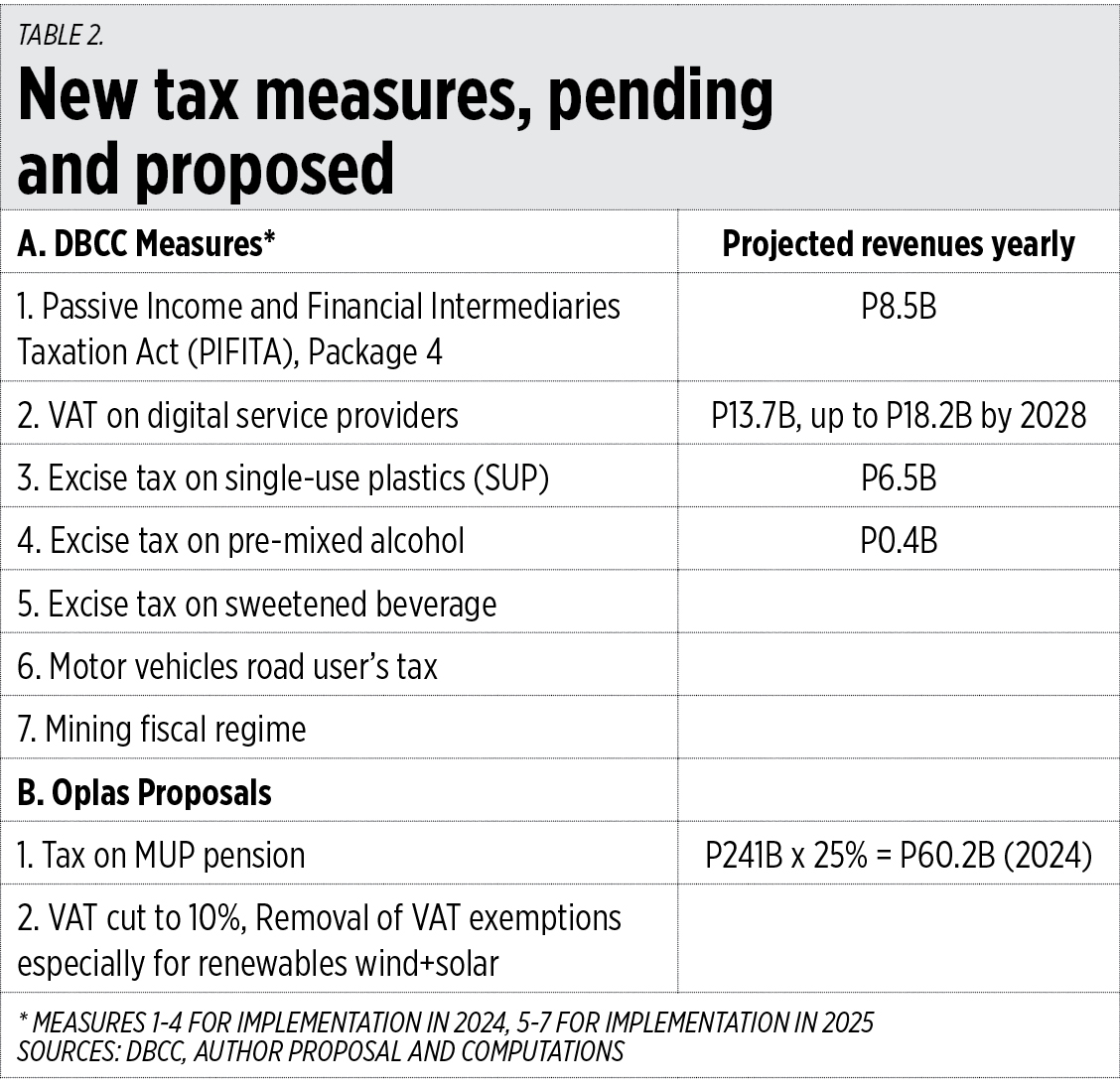

The DBCC has listed seven new tax measures, but they have not yet released updated revenue projections publicly. So, I built this table with projections of some measures mentioned in BusinessWorld. The first four measures are projected to give the government some P29 billion a year.

I add my own two proposals. One, imposing an income tax on military and uniformed personnel (MUP) pension which is big — P160 billion in 2021, P164 billion in 2022, and is projected to be P214 billion in 2023 and P241 billion in 2024, rising further in succeeding years. Currently the MUP pensions are big and tax free.

In 2022, the average monthly pensions were P4,528 for the Social Security System, P13,600 for the Government Service Insurance System, and P40,049 for the MUP. The projected average MUP pension in 2023-2024 would be about P43,000/month and up. This falls in the 25% income tax rate.

My second proposal is to bring the Philippines VAT rate back to 10% from 12%, then remove the VAT exemption of many sectors (see Table 2).

Imposing a VAT of 10% on the sales of renewables will have an upward price effect on power consumers. But bringing down VAT from 12% to 10% for coal, gas, and oil plants, which constitute about 80% of total power generation, will have a price deflation effect for the consumers. Overall, the consumers will likely be better off.

Many MUP pensioners may likely oppose taxation of their pension and they are wrong to do so. First, while in active service they contributed nothing for their own pension; second, their pension comes 100% from taxes and they do not want to contribute to the tax too. This will give them a bad image and public perception that their motto “To serve and protect” refers more to themselves, their superiors, and their pension, and less the public.

The above tax measures should be coupled with spending cuts, borrowings cuts, and, later, tax cuts as the public debt continues to decline. Then more public and private resources will be devoted to more infrastructure, better justice administration, and more business innovations.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers

{kind=link}

{kind=link}