The Philippines is a very small power market by ASEAN standards, with market demand peaking at 15 gigawatts (GW) compared to Thailand’s with 30 GW and Indonesia with 45 GW. This small market is also very fragmented with three major grids, the Luzon grid (12.3 GW as of May), the Visayas grid (2.2 GW) and the Mindanao grid (2.3 GW) being barely connected. The Visayas and Luzon grids are weakly connected via the Bicol-Samar (250 MW) submarine cable. The Mindanao grid was isolated until the Mindanao-Visayas Interconnection Project (MVIP) was energized in May with a starting carrying capacity of a measly 22.5 megawatts (MW). Because of this fragmentation, the Philippines has three Wholesale Electricity Spot Markets (WESM) which many people will say are two too many.

A wholesale electricity market works best if the market is deep with many producers and many consumers on each side of the ledger; markets with few producers means substantial market power and is subject to collusion and price manipulation. Such is the shallowness of the market that one Energy Secretary once bemusedly narrated that one of his duties in the summer months when the power reserve is running low is to call and beg power suppliers for more juice to avoid the politically disastrous brownouts. Such direct contacts between the power authorities and market players is unseemly, even illegal, in a properly functioning market as it facilitates anti-consumer collusion! Which is why many countries in Asia opted to have state-owned and administered rather than competitive power markets. Only the Philippines and Singapore have WESMs in the ASEAN. The plan to properly enable a One Philippine Grid has been in the books since the 1980s.

The story goes that the plan to connect the Mindanao grid to the rest of the country goes very far back but was continuously frustrated by Mindanao politicians and constituencies who opposed the sharing of the then cheap hydropower-generated Mindanao power, back when rainwater was abundant, with the rest of the country (see Boo Chanco’s must read column piece, “Power Failure,” in the Philippine Star on May 19). And the central government — whose duty it was to unbind precisely such conflicts for the common good — could not or would not prevail upon Mindanao to relent; recall this was still under Marcos’ martial law. It was climate change, rainwater scarcity, and a growing frequency of power outages in the island that persuaded the Mindanao constituency to finally relent to the interconnection.

As a panelist at the May 11 Power Module of the Aboitiz Data Institute-sponsored AI Philippines Summit at the Marriot Hotel, in Newport World Resorts we were welcomed by an episode of flickering lights and temporary darkness, but this happily ended a few anxious seconds later. Was it due to a tripping in the National Grid Corp. of the Philippines’ (NGCP) grid which was quickly enough covered by Marriot’s own backup generator (if so, surely fossil fuel-fired) or to some local electrical tripping fortunately covered by Marriot’s own built-in system redundancy? I could not help fearing rolling brownouts because a few days before, on May 6, a Monday, a rolling brownout episode was declared to the dismay of the affected public. And the NGCP reported that the red alert status will continue till June! Why, only on May 3, the Department of Energy (DoE) announced that no red alerts were forthcoming this summer. The red alert and accompanying rolling brownouts were due to several causes: the unplanned electrical problems of coal-fired Calaca units 1 and 2 (equipment malfunction in the complicated fossil-fired units), a tripping incident in the NGCP grid which cut off Masinloc (the NGCP, which seems to prefer its profits going to dividends and not enough to redundancy investment, may be accountable) and force majeure due to a water level deficit in Binga dam (credited to climate change) which stopped power from the Aboitiz Power’s Binga hydro facility. All in all, 1,354 MW was lost to the grid. Energy authorities quickly blamed the non-delivery of power from some gas fired plants and the delay in the delivery of full capacity (450 MW) of the MVIP connecting Mindanao and Visayas. The recently energized MVIP can deliver only 22.5 MW of power of its planned 450 MW full capacity, which the NGCP promises will be realized in December 2023. But wasn’t the MVIP supposed to be delivered even before the pandemic?

These events surprised no one, except the DoE. Every year, in the summer we have, as if by clockwork, red alerts; every year we have congressional hearings to address the problem; every year we continue to host red alerts. Plus ça change, plus c’est la même chose (the more things change, the more they stay the same) seems to be the middle name of this nation in power (but not just).

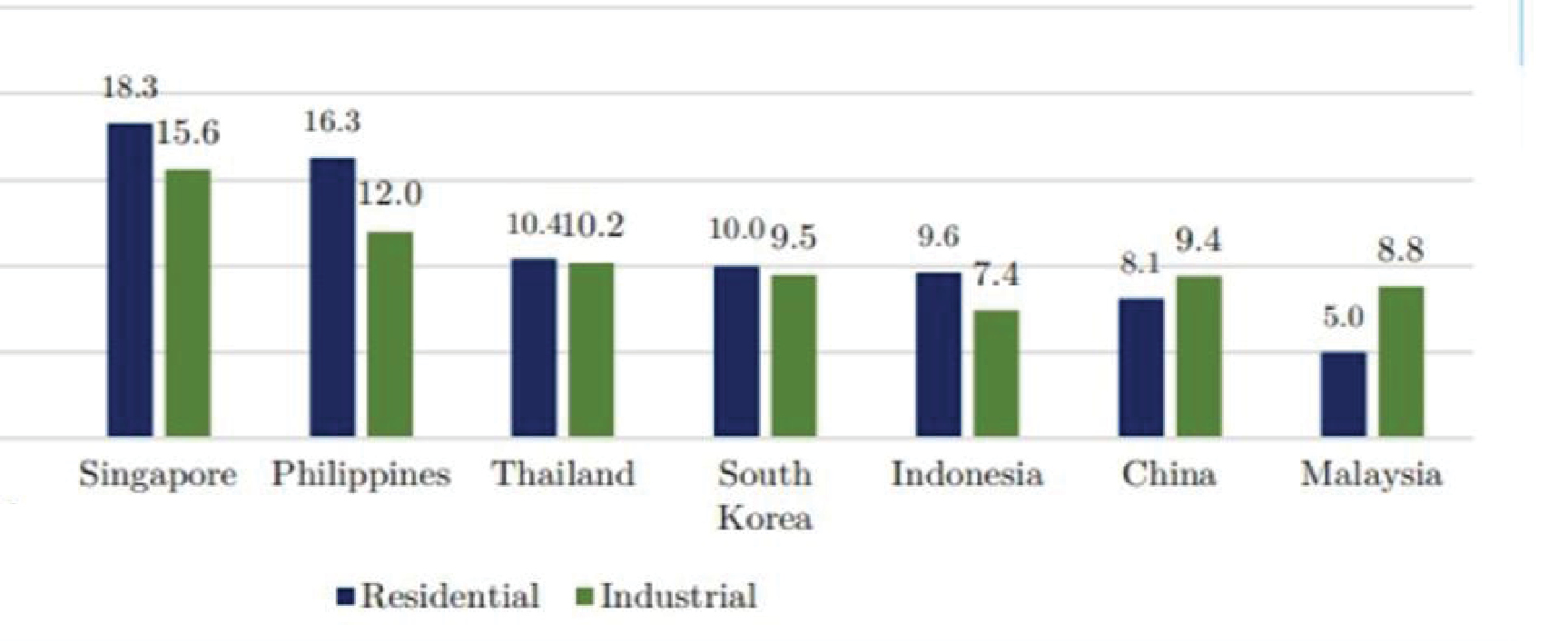

Why is power cost and stability so crucial? Why is the investment rate so low in the Philippines? Power cost is one area where the Philippines leads the ASEAN, barring Singapore. Electricity cost (USc/kWh as of December 2021) charged captive customers by major utilities (from Ravago, 2020) is reflected in the first chart.

Notable are the following:

• The price of power in the Philippines for large business establishment was highest in the ASEAN in 2021 apart from Singapore. But if power supply instability is costed in, stable power “could be more costly” in the Philippines.

• In Malaysia and China, households pay more for electricity than industries!

As a nation we have decided that large businesses subsidize (pay higher than) poor households. The better alternative would have been to use the state treasury to subsidize the poor according to the John Stuart Mill rule: don’t distort the market in pursuit of public welfare goals. Power costs for large establishments are top of mind among investors especially in Manufacturing and export platform investment. The Philippines is kulelat (the far last) as a Manufacturing investment destination in the ASEAN. Better than the Maharlika or constitutional change is the lowering of power costs for business to improve the investment ecology.

The current darling idea for increasing power capacity is nuclear power. Despite the terrible experience with nuclear power (with the Bataan Nuclear Power Plant or BNPP) four decades ago, perhaps we can try it again. Nuclear technology is not static and is now making a comeback with Small Nuclear Reactors (SMRs). Nuclear power has a smaller carbon footprint than even solar and wind. SMRs reactors mounted on ships will have less NIMBY (not in my back yard) problems, and will add resilience to the system better suiting the archipelagic character of the country. A nuclear plant today will boost our power supply. But will it lower power costs? Not if the cost of that additional power is prohibitive. Table 2 shows the cost of electricity (Ravago, 2023) by fuel use.

Worse, the cost of nuclear power has been increasing (up 33%) between 2009 and 2021 while those of renewables have been decreasing (down 90%). Lifespan favors nuclear: nuclear plants last 40 years, solar photovoltaic (PV) panels (30 years), wind turbines (25 years). Renewables are lower on fixed cost and much lower in turnaround time: a decade for nuclear vs 0.5 years for solar. Still, if the private capital decides to wager on nuclear plants with its own resources, go ahead.

There is a segment of solar renewables that is even more attractive: solar panels on idle rooftops. No NIMBY problems, no land use displacement issue; no environmental assessment hurdles, quick turnaround time (solar power starts to flow in six months). Furthermore, rooftop solar electricity will not be burdened by grid and local distribution cost; no universal, feed-in, and stranded asset levees; and can help shave demand. When matched with battery storage it can help stabilize the grid. Renewable power is the un-paralleled low-lying fruit we must optimize in this decade.

Policy Recommendations:

1. Existing large establishments could be required to gradually replace fossil fuel backup generators with grid-scale batteries.

2. New establishments could be required to acquire battery storage-based backup in lieu of fossil fuel fired back-up.

3. Add as a permitting requirement for new buildings a rooftop solar panel installation.

4. Make solarized residences the default option for residential buyers (“opt out” if you don’t want to be “solarized”).

5. Contingent idle rooftop tax: an x% tax on idle rooftops (per square meter of roof) for all top 500+ corporations; “contingent” because the tax is automatically lifted once the firm generates in situ y% of total consumption through rooftop solar PV generation.

6. Slowly shift the household subsidy burden from Manufacturing to Services and the national treasury.

Let’s put our renewable power program on speed dial.

Raul V. Fabella is a retired professor of the UP School of Economics, a member of the National Academy of Science and Technology, and an honorary professor of the Asian Institute of Management. He gets his dopamine fix from tending flowers with wife Teena, pedal-powering a bicycle, and assiduously, if with meager success, courting the guitar.

{kind=link}

{kind=link}

{kind=link}