The Cha-cha train continues to chug confidently along even after President Ferdinand “Bongbong” Marcos, Jr. (BBM) confessed disinterest. The bone of contention is the lifting of the constitutional restriction on foreign ownership which, advocates loudly claim, will open the floodgates to foreign investment. Congress, it seems, is betting that when presented with a prospect of gratuitous tenure extension, President BBM would not veto the prospective Cha-cha (charter change) law. For one, there is no foolproof guarantee that only the foreign ownership restriction will be lifted; two, why only the foreign ownership restriction? The farm size ownership restriction to five hectares and to the tradability of farm lands associated with CARP (Comprehensive Agrarian Reform Program) and the Constitution are just as, or even more deleterious, to overall investment than foreign ownership restriction. And overall investment, not just foreign investment, should be our concern.

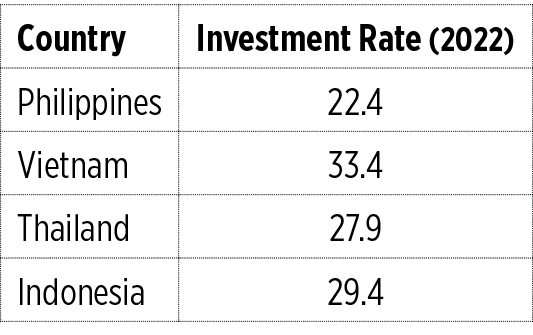

Our overall investment record is tawdry. That metric of concern is the investment rate — the share of investment (GDCF) in GDP. GDP finances both consumption and investment. Investment is what finances a better tomorrow. For 2022, we juxtapose the Philippines’ investment rate with selected nearest rivals (see table).

Two years after we passed the CREATE 2 Law (Package 2 of Corporate Recovery and Tax Incentives for Enterprises Act) in 2020 ostensibly to incentivize investment by corporations, the Philippine investment rate remains the lowest among our nearest rivals. We prefer to consume now rather than build up our children’s future. Our annual investment rate has not breached the 25% annual standard which separates the thoroughbreds and the laggards in the development highway. CREATE 2 was sold to the Filipinos as a “game changer” adding to the litany of many game changers in the past: the capital account liberalization, the World Trade Organization accession, the retail trade liberalization, etc. But our investment rate has stubbornly remained between 20-24%.

Why has our investment rate and our share of foreign investment in the ASEAN remained impervious to these so-called “game changers”? Why have the promised tsunamis failed to roll to our shores?

COMPETITIVE ECOLOGYThe reason is that investment responds not to piecemeal policy changes but to drastic changes in the investment ecology. By investment ecology I mean a battery of policies (fiscal, monetary exchange rate, regulatory policies, and quality of the rule of law), all supporting the same general direction. Stable macro will get you nowhere if many sectors are closed to investors (say, the farm sector or mining). CARP sees to it that large capital investors will keep clear of farm and food production.

Where contracts are not enforced and/or property rights are undefined, thus, unprotected, investors go elsewhere. The industry-scale swine project of San Miguel Food Corp. in Sumilao ran into a firestorm of indigenous rights and CARP rules in 2007 that only the enormous resources of San Miguel Corp. could afford to navigate. The message for potential food investors was “Beware!”

Where the rule of law is weak, the appetite to investment sours. But even if the rule of law is adequate, investment in power-intensive activities will shy away if the cost of power is prohibitive.

To be dead-shot competitive, one’s investment ecology must exhibit a modicum of all the requisite features. Improvements in some while other features remain below modicum will harvest only the dregs: the least beneficial types of foreign investment.

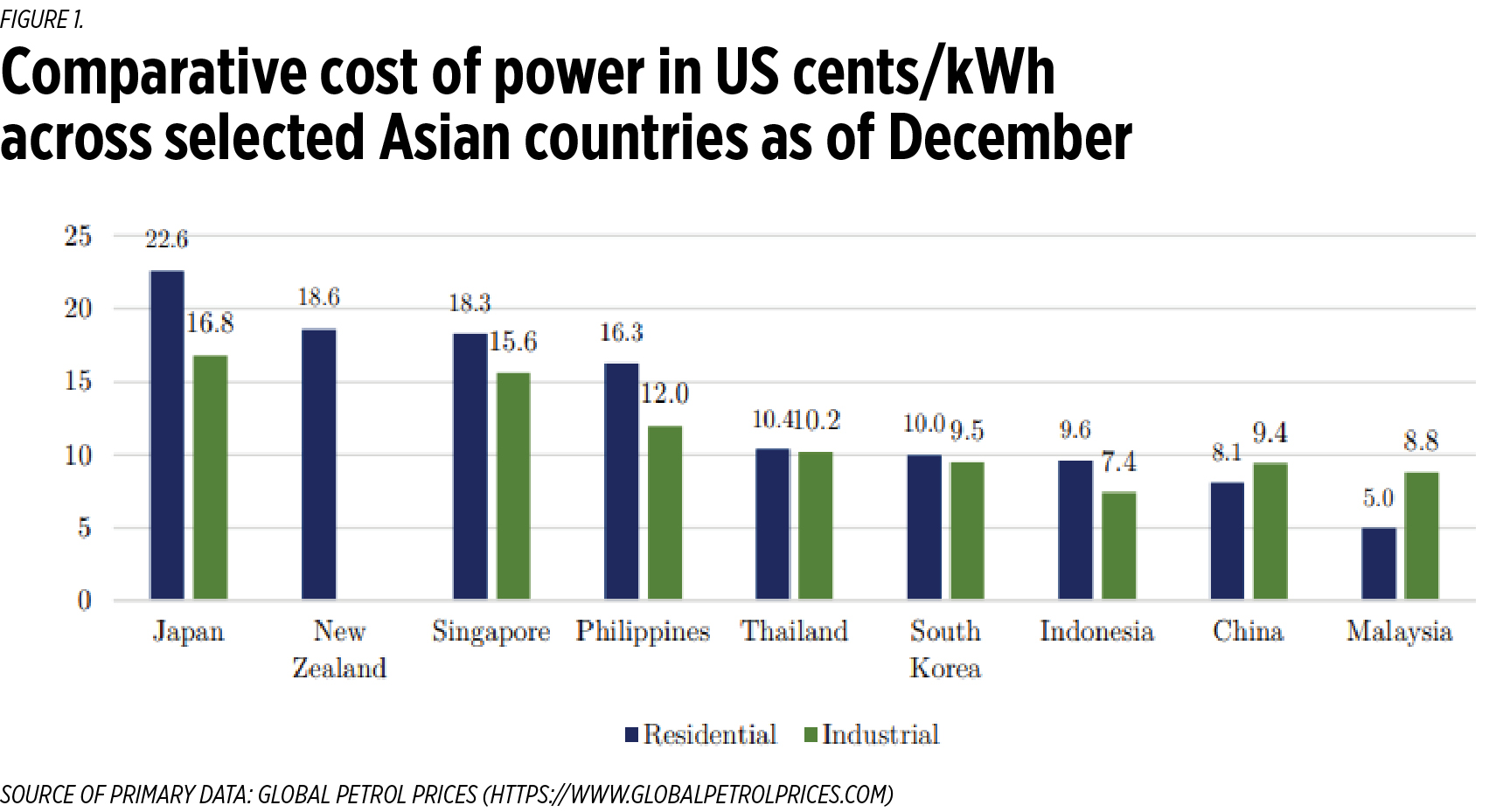

And power in the Philippines is indeed very costly relative to rivals. Figure 1 shows the comparative cost in US cents/kWh (kilowatt hour) across the selected Asian countries as of December 2021 (lifted from Ravago, 2023).

The Philippines has the highest power cost both for Industrial and Residential in the ASEAN barring Singapore. If reliability is factored in, the Philippines’ tariffs may exceed that of Singapore. The difference between Industrial and Residential tariff is highest in the Philippines (4%). In Malaysia and China, residential tariff exceeds industrial tariff! We have the lowest per capita generation of electricity (885 kWh 2020 vs. Thailand’s 2,531 kWh, Indonesia’s 1,004 kWh, and Malaysia’s 4,695 kWh), resulting in our per capita consumption (which is megawatts/cap or mWh/cap = 0.90) being the lowest in the region and below the notional power poverty threshold (1 mWh/cap). The periodic red and yellow alerts and/or actual rolling brownouts in the summer months shows that our power reserve is too thin. These disruptions raise the nominal and effective price of electricity.

Power is a very important — for some the most important — feature of the investment ecology. Investors in manufacturing and platform exports especially look at relative power cost. Asian economies falling flat on power cost will fall flat on investors. That is the Philippines’ sad plight.

In the Philippines, our lawmakers are feverishly wasting time arguing over Cha-cha and the Maharlika Investment Fund as attractions for foreign investment, while power cost and the rule of law far outweigh these as standard operating procedures for investment, both local and foreign.

Of course, foreign investment is of many varieties, not all of them healthy for the economy. Some don’t care for power cost and hardly for the rule of law. In the 1990s, we liberalized our capital account (made bringing in and out of capital easier) ostensibly to attract more foreign investment. We had some flocking but what variety did we get? Not of Direct Foreign Investment (DFI) that generates long-term employment and income, but of portfolio investment in pursuit of arbitrage — vulture capital, which are here-today-gone-tomorrow after they clean up. The ratio of portfolio to DFI is highest in the Philippines (up to 120% vs. 25-50% in the Asean in some years).

How about local capital? The high cost of power sent them taking cover in the non-traded goods sector (property, CBD, retailing) where they do not compete with the global rivals. So, what are we doing to lower our power cost?

Among others, the Nuclear Energy Program (NEP). The government and Department of Energy are seeking relief from nuclear fission technology to augment our baseload capacity. But the price outlook is not good for nuclear power vs. other fuels. It is especially inferior to renewables (five times cheaper than nuclear according to Lazard Investment Bank). If the NEP target is 600 megawatts of additional power in nine years at the cost of $1 billion, renewables especially solar, can easily deliver that at much lower cost.

How about the elephant in the room called intermittency? The “blended price” of solar power or the price of “solar plus battery storage” power, meaning “baseload solar” is now still lower (Lazard Investment Bank, LCOE July 2022) than nuclear. Nuclear plants can increase power supply but if at a higher cost, our power cost may rise. Furthermore, solar photovoltaic-generated power can start flowing in six months, not six years.

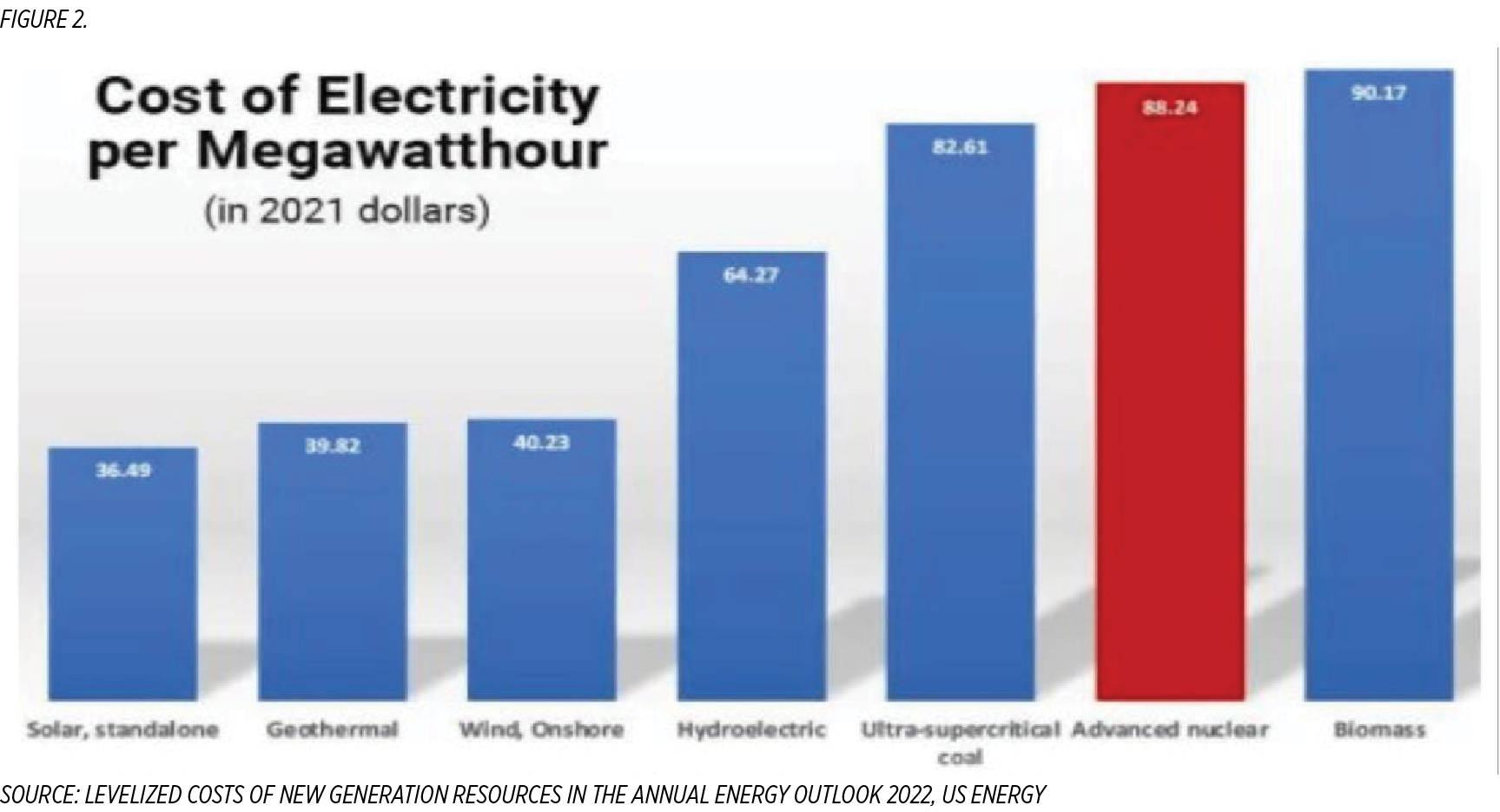

The urgency of lowering power cost in our investment ecology is not debated. But additional supply will not lower the power cost if the cost is prohibitive. Nuclear is not cost-competitive; renewables-plus-storage is, and with the prospect of rapid further decline. Figure 2 (from Mathews, 2022) shows that the LCOE (levelized cost of electricity, or the average cost in currency per energy unit) of nuclear in 2022 is way higher than solar and wind. It could only worsen, not solve the problem.

But even more auspiciously cheaper is the solar photovoltaic generation mounted on idle rooftops owned by large corporations — no NIMBY (not in my back yard) problems, no transmission and distribution charges, no missionary and universal charges, since the power is not going to the grid. It is modular and can start small. Kudos to the Gokongwei Group for realizing this, becoming a power company from solarized roofs (31-megawatt capacity).

The country gave Philippine corporations a tax break (to 25% from 30% corporate income tax) in the hope that they would deploy the savings for new investments to speed up economic recovery. They did not. It was just a massive transfer of resources to the rich, the big capital owners. Our investment rate has remained below 25%.

Congress should consider passing a “contingent idle rooftop tax”: a nominal tax of x% per m2 on idle rooftops owned by top 1,000 corporations which tax is lifted automatically once the company generates 20% plus of its total consumption by rooftop-mounted solar PV. And while at it, Congress may also consider lifting the universal and FIT charges the way Germany does.

Let’s get our investment ecology air-born.

Raul V. Fabella is a retired professor of the UP School of Economics, a member of the National Academy of Science and Technology, and an honorary professor of the Asian Institute of Management. He gets his dopamine fix from bicycling, assiduously wooing the guitar despite meager success, and tending flowers with wife Teena.

{kind=link}

{kind=link}

{kind=link}