I am pleased to share with readers the summary of our March 3 quarterly forecast report for Globalsource Partners subscribers, mostly global asset managers and banks. Globalsource Partners (globalsourcepartners.com) is a New York-based network of independent analysts doing macroeconomic and political risk analyses of emerging markets. Christine Tang and I are their Philippine advisors.

Much like the last Year of the Rabbit 12 years ago, we enter 2023 as if going down a rabbit hole, not quite sure if surprises ahead will be the pleasant or biting sort. As in 2011, 2023 follows a year of stunning above 7% GDP growth and like before, the question we are struggling to answer now is whether momentum can be sustained and how strongly. The year 2011 turned out worse than expected with only a 3.9% GDP growth rate due mainly to the then new administration’s political choices that the current government is set to avoid.

Fast forward to today, early gauges of domestic economic activity — e.g., PMI, car sales — suggest that there is momentum going into 2023 as memories of the pandemic fade. The global outlook has also become less gloomy with advanced economies showing resilience and China reopening after exiting its zero-COVID policy. The latter bodes well for Asian economies like the Philippines eyeing a rebound in tourism.

On the other hand, most of the factors underpinning our sober outlook last quarter still hold. Externally, world economic growth is still expected to weaken following the series of jumbo rate hikes last year and downside risks still dominate. Locally, high inflation has persisted, monetary policy is expected to remain contractionary, and fiscal policy, on a consolidation path. Although the economy still has remittances and BPOs (including gig workers) to fall back on, the large windfall from last year’s dollar rally has disappeared.

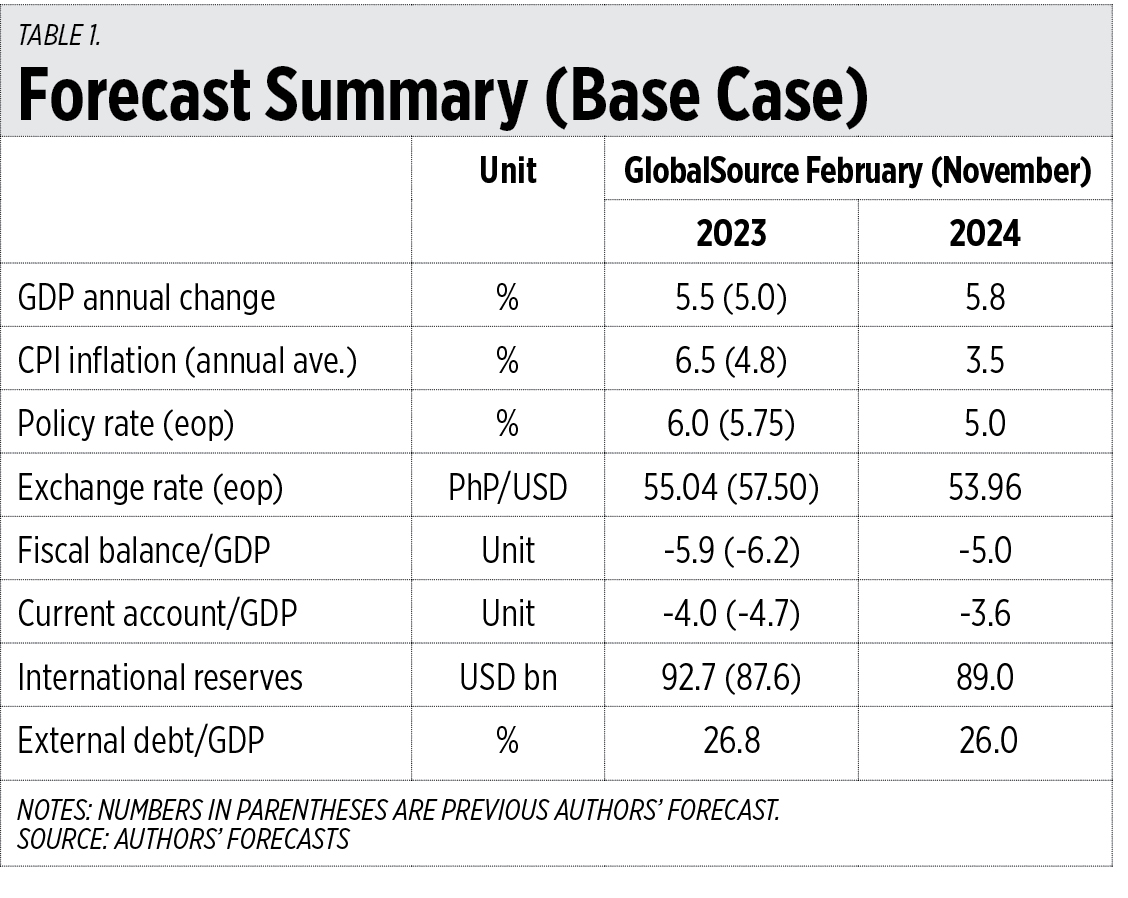

Weighing these against the new developments, we have decided to bump up our 2023 growth forecast by 0.5% to 5.5% on the strength of lingering catch-up demand and inbound tourism. This upgrade is still below government’s 6% low-end target and assumes that it keeps to its promise of spending the equivalent of 5% of GDP on infrastructure. The forecast comes with major downside risks. Locally, most notable are, a.) continued lapses in the management of food supplies that have contributed to skyrocketing prices of basic goods, and, b.) the President’s upcoming choice for BSP (Bangko Sentral ng Pilipinas) governor, critical for preserving similar confidence that markets have on the incumbent, as well as possible mid-year changes in the cabinet. The external outlook also faces risks from more turbulence in financial markets, elevated and volatile commodity prices, trade disruption due to heightened US-China tensions, and a resurgence in COVID cases.

On the upside, the Senate’s recent ratification of the Regional Comprehensive Economic Partnership (RCEP) as well as closer security ties with the US could see the beginnings of friend-shoring investments trickling in.

Romeo L. Bernardo is a co-founder, trustee/director of the Foundation for Economic Freedom. He serves as a board director in leading companies in banking and financial services, telecommunication, energy, food and beverage, education, real estate and other. He has had a 20-year run in the public sector including stints in the Department of Finance (Undersecretary), IMF, World Bank and the ADB

romeo.lopez.bernardo@gmail.com

{kind=link}